Penticton Housing Market Update – May 2026

May built on April’s momentum. Sales activity strengthened again, dollar volume climbed, and for the second month running the market is showing real signs of life after a slow start to the year. The broader backdrop stays cautious, though, with a soft national economy and borrowing costs holding steady, and as always the local numbers tell a more nuanced story than any single headline.

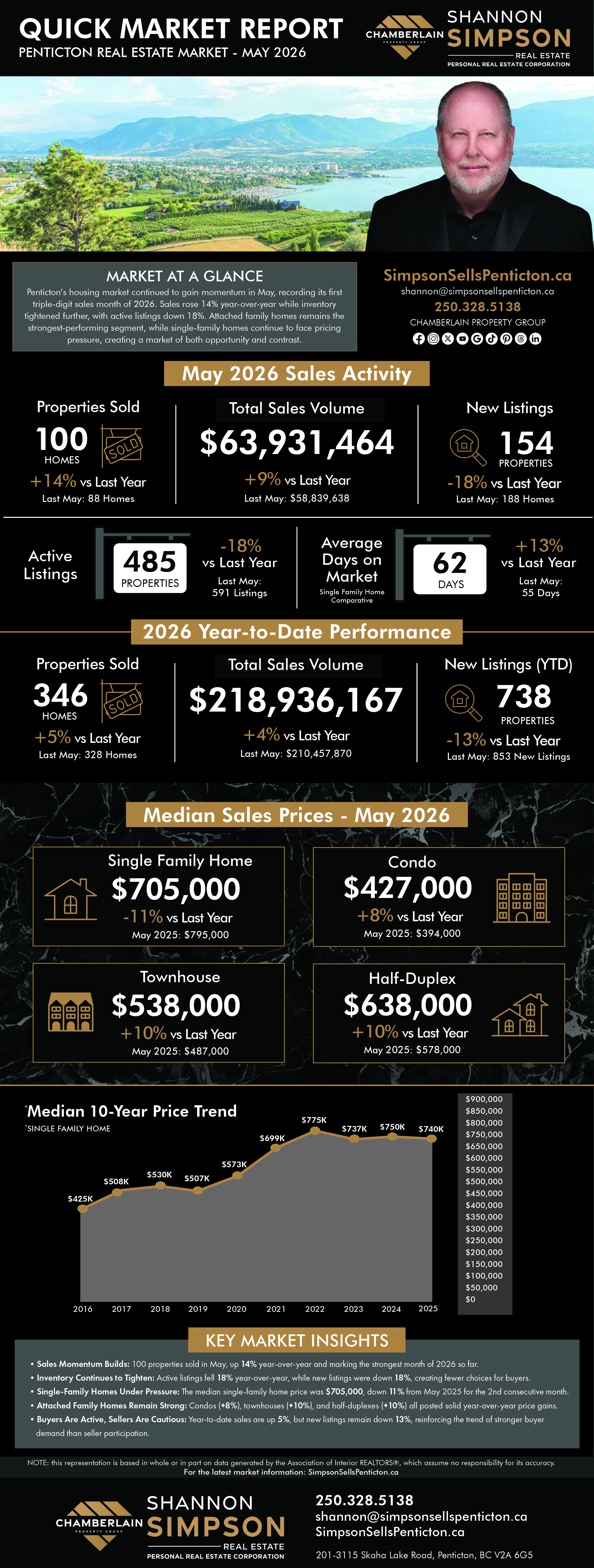

Penticton recorded 100 sales in May, up 14% from 88 in May 2025, with total dollar volume reaching $63.9 million, a 9% increase over last year’s $58.8 million. This was the strongest month of the year so far, and the first time monthly sales have reached triple digits in 2026. Notably, dollar volume rose less than unit sales this month, the reverse of April, which points to more activity at moderate price points rather than at the top end. On the supply side, 154 new listings came to market, down 18% from 188 a year ago. Year-to-date, 346 properties have sold, up 5% over the same period in 2025, with cumulative dollar volume of $218.9 million, up 4%. New listings for the year sit at 738, down 13% from 853 at this point last year. The theme that has held through the first five months of 2026 is unchanged and, if anything, sharper: buyers are showing up, but sellers continue to hold back.

Prices and Property Types:

- Single‑Family homes: Median price sits at $705,000, down 11% from $795,000 last May. This is the figure that continues to demand attention. While the median ticked up about $17,000 from April’s $688,000, the year-over-year decline held firm at 11% for a second straight month. That consistency matters: it tells us the softness in detached pricing is a trend, not a one-month anomaly.

- Condos: Median price at $427,000, up 8% from $394,000. Another solid year-over-year gain that holds the pattern of relative strength in the entry-level attached segment, though slightly below April’s $435,000 in absolute terms.

- Townhouses: At $538,000, up 10% from $487,000. Still gaining, and still the segment to watch, though the pace cooled from April’s striking 16% year-over-year jump. The absolute median rose again month-over-month, which suggests genuine, durable demand rather than a one-time spike.

- Half Duplexes: $638,000, up 10% from $578,000. Consistent with the now-familiar story that attached housing across the board is holding and gaining while detached softens.

The split between single-family and attached pricing remains the defining feature of this market, and May reinforced it rather than resolving it. All three attached categories posted solid year-over-year gains while detached fell 11% for the second consecutive month. Buyers priced out of, or simply wary of, single-family homes are continuing to find value in townhouses, condos, and half-duplexes, and that demand keeps showing up clearly in the numbers.

Market Pace and Inventory:

Single-family homes averaged 62 days on market in May, up from 55 days last year, a 13% increase, and up from 54 days in April. Detached buyers are clearly taking their time, which fits the pricing pressure in that segment. Active inventory sits at 485 listings across all categories, down 18% from 591 at this time last year. With new listings also down 18% for the month, the supply contraction that has defined 2026 deepened further in May. Fewer homes are coming to market, and the overall pool of choices keeps shrinking.

What This Means for You:

- For sellers: If you’re selling an attached property, townhouse, condo, or half-duplex, May’s numbers remain encouraging. Demand is steady, prices are holding their year-over-year gains, and well-presented listings are moving. If you’re selling a single-family home, the message has not changed: pricing has to reflect where the market actually is, not where it was a year ago. Two consecutive months of an 11% median decline is not noise, and optimistic pricing in this segment will be met with longer days on market, not higher offers.

- For buyers: Inventory keeps tightening, down 18% year-over-year, and the attached segments are competitive. The flip side is that single-family pricing has genuinely softened, which is creating opportunity for buyers who are ready and financed in that category. Borrowing costs have been stable for months, which makes planning easier, but stability is not the same as stimulus. Patience still has value in detached homes; it has a shorter shelf life in townhouses and condos.

- For everyone: May’s data reinforces what has now been building for half a year. This is not a uniform market, and it is not a market that rewards assumptions. It behaves differently depending on property type, price point, and neighbourhood, and it is unfolding against a national economy that remains soft. Decisions made without understanding those distinctions are decisions made with incomplete information.

My Take:

May was the most active month of the year, and the headline is a good one: 100 sales, the first triple-digit month of 2026, with dollar volume up 9%. After a hesitant winter, two straight months of building activity is a real and welcome signal. But I’d temper the optimism with the same caveat I raised in April, because the data is raising it again.

The single-family median fell 11% year-over-year for the second month in a row. One month of that could be a fluke of which homes happened to sell; two months in a row is a pattern. In a market where inventory is down 18% and would ordinarily push prices up, the fact that detached pricing keeps softening tells me there is a real ceiling on what buyers in that segment can or will pay. That ceiling is tied to affordability and financing. The Bank of Canada is widely expected to hold its key lending rate at 2.25% at its June 10 decision, a fifth consecutive hold, so borrowing costs are not getting meaningfully cheaper any time soon, and detached pricing is reflecting that reality.

The wider backdrop is worth keeping in view. The national economy contracted slightly in each of the first two quarters of the year, and a recent spike in energy prices has added a layer of uncertainty to the inflation picture. None of that is a Penticton-specific problem, but it shapes the overall mood and it is part of why the Bank is sitting on its hands. Locally, the number I flagged last month, the townhouse segment, is still climbing, just at a calmer 10% rather than April’s 16%. I read that as healthy: a steady, sustainable gain is more reassuring than a one-month surge, and it confirms that attached housing is where buyer demand is genuinely concentrated right now.

The year-to-date picture, up 5% in unit sales and up 4% in dollar volume, is modestly better than April’s read and points to a market that is gradually outperforming last year rather than dramatically so. Spring delivered, two months running. The real question for June and into summer is whether this is durable momentum or simply the seasonal bump arriving on schedule. Either way, May was a genuine step forward, with the same honest caveat attached: the detached segment is still searching for its floor.

Remember, if you have any questions, I’m always here to help you MAKE SENSE OF IT ALL!